In the evolving landscape of corporate accountability, the Corporate Sustainability Reporting Directive (CSRD) represents a paradigm shift in how sustainability performance is disclosed, assessed, and integrated into strategic business decisions. Replacing the Non-Financial Reporting Directive (NFRD), the CSRD not only broadens the scope of reporting obligations across the European Union but also aligns environmental, social, and governance (ESG) metrics with broader financial transparency and risk assessment frameworks.

This deep dive unpacks the objectives, scope, reporting standards, and implications of the CSRD, providing sustainability professionals and reporting entities with a foundational understanding of this regulatory milestone.

The NFRD, adopted in 2014, was a critical first step in mandating ESG disclosures by large public-interest companies. However, its limited applicability—covering approximately 11,000 entities—and inconsistent reporting practices highlighted the need for more robust and standardized sustainability reporting mechanisms.

In response, the European Commission introduced the CSRD as part of its European Green Deal and Sustainable Finance Strategy, with the goal of:

The CSRD applies to:

Over 50,000 companies are expected to fall under the CSRD regime—up from 11,000 under the NFRD.

The CSRD requires limited assurance over reported sustainability data, transitioning eventually to reasonable assurance. This brings ESG reporting closer to the rigor of financial audits.

Reports must be prepared in XHTML and tagged using XBRL, ensuring compatibility with the European Single Access Point (ESAP).

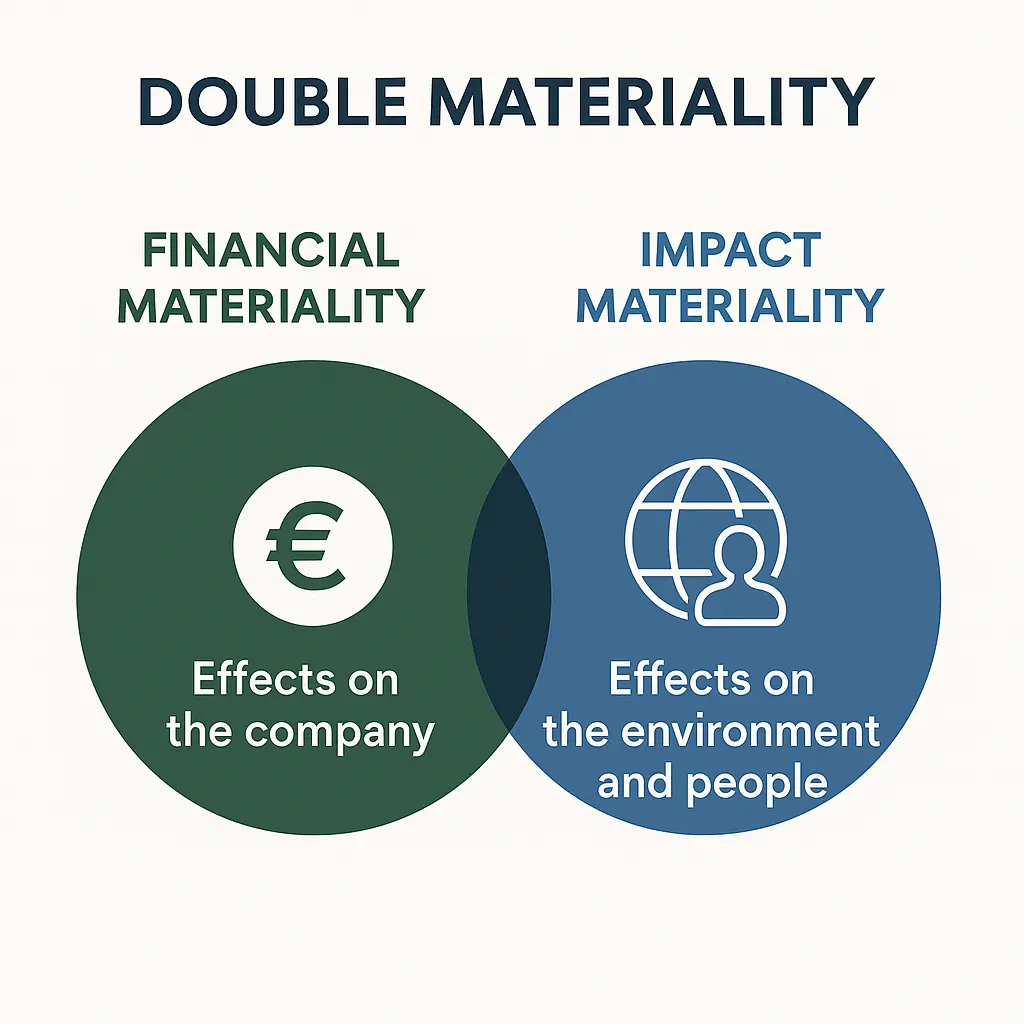

The CSRD enshrines double materiality as a central concept:

This dual approach emphasizes accountability in both risk and impact terms.

Reporting must follow the European Sustainability Reporting Standards (ESRS), developed by EFRAG, including:

| Year | Applicability |

|---|---|

| 2024 | Companies under NFRD |

| 2025 | Other large EU companies |

| 2026 | Listed SMEs |

| 2028 | Non-EU companies with EU operations |

Sustainability must now be integrated into corporate strategy, not treated as an isolated function.

Meeting CSRD requirements demands ESG expertise, internal controls, and collaboration across finance, compliance, and sustainability teams.

High-quality disclosures enhance stakeholder trust, and access to green financing instruments such as bonds and sustainability-linked loans.

Potential hurdles include:

Nonetheless, the CSRD may drive convergence toward a global ESG baseline.

The CSRD signals a transformative moment for corporate transparency. More than a regulatory tool, it is a framework for embedding sustainability at the heart of corporate value creation. Organizations that prepare early will not only avoid compliance risk but also strengthen their strategic positioning in the global sustainability transition.